The Reverse convertible is the simplest and oldest form of a yield enhancement structured product.

An example of such a product is defined by the following elements:

- Issuer : Bank ABC

- Maturity : 18 months

- Underlying : Microsoft Corp (MSFT)

- Currency : USD

- Denomination : 100,000

- Coupon rate : 5% per annum

- Coupon Frequency : quarterly

To make the description of the payoff easier, let’s note S(t) the price of the underlying S at time t.

S(0) will then ben the price the underlying at time 0.

S(T) will be the price of the underlying at maturity.

The payout of such a product will be (and subject to the issuing bank ABC not defaulting) :

- During the life of the product

The coupon of 5% per annum will be paid on a quarterly basis (1.25% per quarter). That coupon is guaranteed in the sense that it is paid irrespective of the performance of the underlying security (here Microsoft) - At maturity, the redemption of the note will be

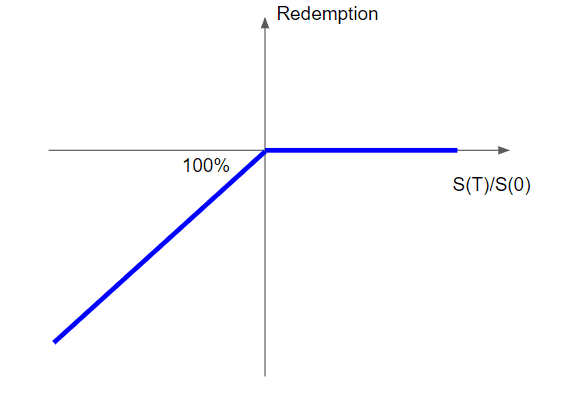

- 100% if S(T) is greater or equal to S(0)

- S(T)/S(0) if S(T) is strictly less than S(0)

Graphically, here is the redemption of the redemption at maturity, ignoring intermediary guaranteed coupons

Once can recognize the payout of a short put position, indeed for the investor, buying a reverse convertible is equivalent to

- Being long a zero-coupon bond issued by the issuing bank

- Receiving regular guaranteed coupons from that issuing bank

- Being short an at-the-money put option on the underlying security